Letters of Credit: Problem Solvers and Opportunity Generators

By John “JJ” Jaravata, Associate Director, Member Services Trader

In this first of a series of articles spotlighting Letters of Credit, we explore the steady rise in the use of FHLBank San Francisco’s Letter of Credit (LC) product for Public Unit Deposits.

Our LCs can be used to solve problems, such as a lack of suitable, highly liquid collateral, or to support new or expanded business activities, such as liability or asset generation. The most popular use of LCs by our member financial institutions is to secure Public Unit Deposits (PUDs) under various state and local agency deposit programs, both within the Bank’s district of Arizona, California, and Nevada, and in certain other states.

Our LCs can be used to solve problems, such as a lack of suitable, highly liquid collateral, or to support new or expanded business activities, such as liability or asset generation. The most popular use of LCs by our member financial institutions is to secure Public Unit Deposits (PUDs) under various state and local agency deposit programs, both within the Bank’s district of Arizona, California, and Nevada, and in certain other states.

For an FHLBank San Francisco member already taking PUDs, the LC can be a more attractive form of collateral for both our member and their depositor customer. For members not already offering PUDs, the LC might be considered an ideal form of collateral for taking advantage of this desirable source of funding and vehicle for community involvement.

What is an LC and what purpose does it serve?

An LC guarantees payment to the beneficiary in the event a member does not perform its underlying obligation. In the case of an FHLBank San Francisco-issued LC, it bears our AAA / AA+ credit rating. As a form of collateral or credit enhancement, this rating makes it especially valuable to the beneficiary.

Until recent liquidity regulatory changes, the more common practice for those active in PUDs was for the financial institution receiving the deposit to collateralize the subject deposits with eligible securities for the benefit of the depositing municipality or local agency. These pledged securities would be held by a custodial bank or trust as the agent of, and custodian for, the municipality or local agency. The financial institution receiving the deposit would then be required to provide detailed collateral reports to the depositor. In the event of the non-return of the deposit, the securities would be liquidated, and the proceeds paid to the depositor.

But when using our LC as collateral, FHLBank San Francisco would make the payment, upon demand, to the municipal or agency beneficiary, and no securities or loans would need to be sold. Using our LC as collateral is simpler, there is less operational risk, and our member avoids some of the disadvantages of using securities (custody, reporting, valuation, liquidation) as collateral.

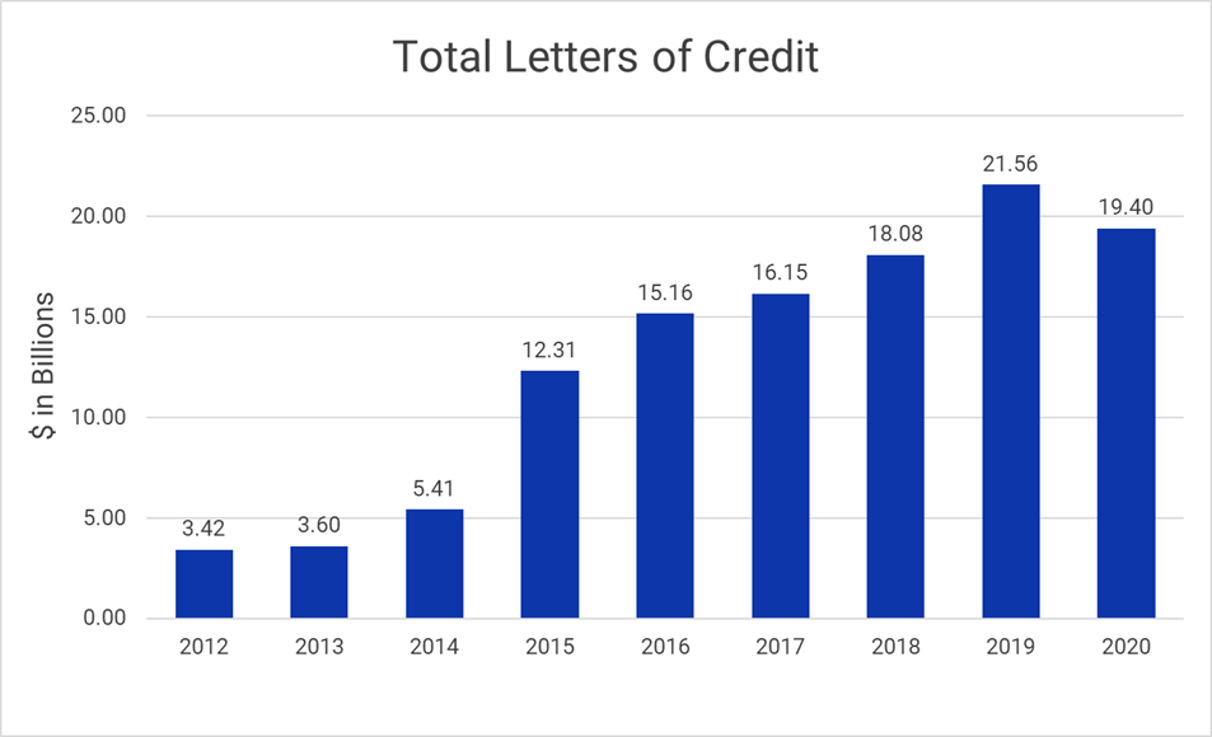

The dramatic increase in the Bank’s volume of LC transactions, shown in the following chart, is almost entirely due to how the use of our LCs to support PUDs, in multiple states, has grown in popularity.

Let’s explore the benefits and characteristics of the FHLBank San Francisco LC in a little more detail.

A Letter of Credit is defined as an independent, irrevocable obligation of the Bank to pay the beneficiary if the member does not perform its underlying obligation to the beneficiary. One of the features that makes it so valuable as collateral is that it is “Irrevocable,” which, apart from the word being a fun and impressive thing to say, means that the LC cannot be altered without the consent of the beneficiary.

Use of our LCs for PUD’s can result in:

- Improved liquidity: For regulatory purposes, once securities are pledged, they cannot be factored into liquidity ratios. It makes sense to pledge less liquid whole loans to FHLBank San Francisco to support the issuance of an LC to preserve your securities portfolio for liquidity purposes.

- Reduced interest rate risk: A low interest rate environment has made holding securities less attractive.

- Reduced operation risk: Managing portfolios of securities as collateral demands significant operational and reporting activities that are not necessary with LCs.

Additional features and benefits include:

- Issuance fee of $100

- Annual maintenance fee of 10 bps

- There is no cost to the Public Unit Depositor

- Amount of LC is tailored to your request

- No minimum size

- Amount can be modified, and term adjusted, with approval of beneficiary

- FHLBank San Francisco is AAA rated by Moody’s and AA+ by Standard & Poor’s

- Simple documentation

- Online application and same day issuance, if requested before 12pm PST

If you’d like to develop or expand this attractive deposit program by marketing our Letter of Credit to prospective clients, download our one-page LC product profile or this more detailed presentation.

In our next issue of Bank Notes, we will highlight how our LCs can be used to support multi-family lending.

Questions? Contact your Relationship Manager or call the Member Services Desk at (415) 616-2500.